Grounded’s Airbnb: From a Housing Problem to Solution report looks at the impact of Short-Term Rental (STR) on communities in Australia’s tier one tourism towns.

The report recommends an innovative cap ‘n trade approach to rebalance the market towards long term trends.

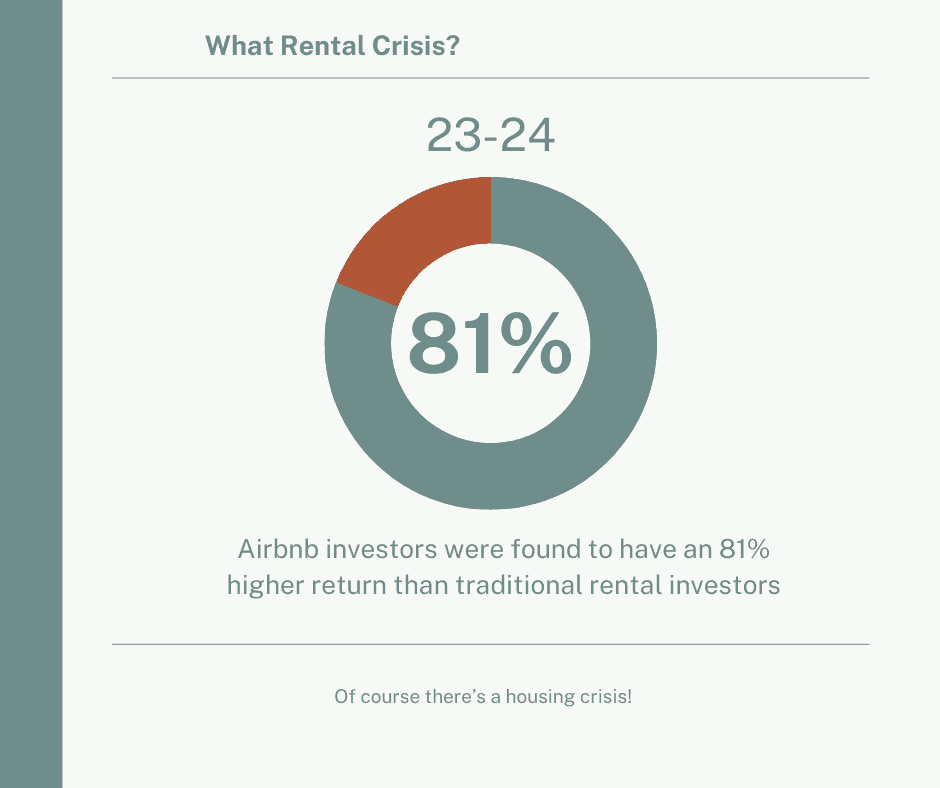

Short term rentals such as Airbnbs have enjoyed an 81% higher return than investing in the long term rental market. This is driving the growth in STRs, with the equivalent of 74% of new housing supply heading straight towards Airbnb (decade to mid ‘24).

This has magnified the challenges renters and home buyers face in the never ending housing crisis.

Key findings:

- $584.6m in net profits was enjoyed by STR owners.

- The 11,935 STRs delivered an average net profit of $48,980 each p.a.

- Net returns were 80.9% higher for STRs over LTRs.

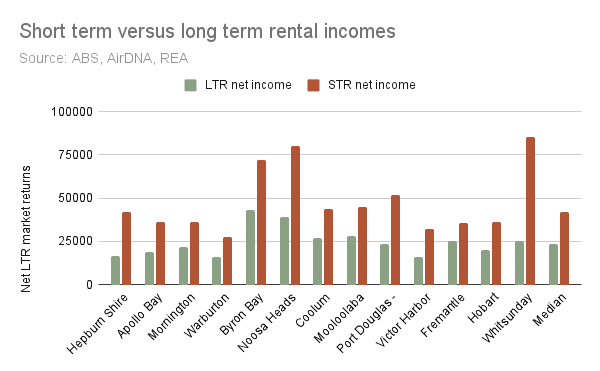

- STRs in the Whitsundays were most profitable at $60,125 p.a above LTRs

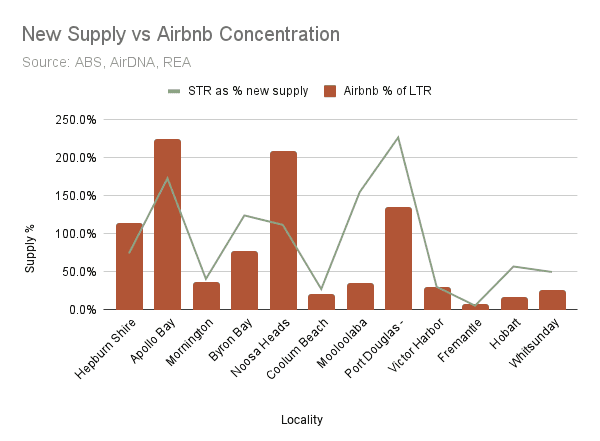

- 74.2% of new housing supply was directed towards STRs across the 13 locales.

- Hepburn Shire, Byron Bay, Apollo Bay and Noosa Heads had more STRs than LTRs

- These localities saw STRs consume housing supply at a rate of 118%.

- The concentration rate of STR was extenuated in Apollo Bay (224%) and Noosa Heads (208%) where STRs were more than twice the LTR supply.

- STR owners shared in a median $33.6m in economic rents (super profits) per locale.

Twelve thousand STR properties were analysed across Hepburn Shire, Mornington Peninsula, Byron Bay, Fremantle, Victor Harbor, Hobart, Noosa Heads, Coolum Beach, Port Douglas, the Whitsundays, Warburton, and Apollo Bay.

The median earnings difference between STR and LTR was just over $17,000. The Whitsundays earnt 237% more than LTR investors, with Hepburn second at 150%.

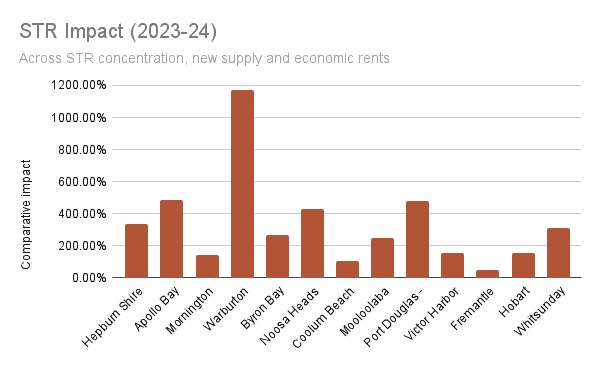

The study ranked towns according to the profitability and saturation of STRs to LTRs, alongside the absorption of new housing supply into STRs.

A combination of pressure points was used to calculate the most impacted communities in our study. The top 5 most impacted communities were:

- Warburton

- Apollo Bay

- Port Douglas

- Noosa Heads

- Hepburn Shire

Apollo Bay and Noosa Heads both had twice as much stock on the STR market as the LTR rental market. Warburton had next to no new supply, but STR had accelerated at a dramatic rate, taking away from existing rentals.

We were surprised to see Byron Bay coming in at no 7, showing how much pressure exists across our tier one tourism towns, both now and into the immediate future.

The return on investment in STR will see more supply heading that way unless the government takes action. A Locals First Airbnb Cap n Trade system must be implemented to both curb the growth in STRs whilst giving the most marginal STRs time to redeploy resources.

Through this STR licensing system, Airbnb could improve its social licence by helping to address the problems at source. The 13 local councils could benefit from a potential $143m in revenue, with the funding of Community Land Trusts preferred so that perpetually affordable housing could be established.

The Airbnb Cap ‘n Trade system

The supply of STRs must be capped immediately. Even though the STR market is slowing, we can expect many communities to further endure the pursuit of short term profits that airbnbs enable.

The policy centres around:

- The creation of STR licensing permits

- A cap on the number of STR properties per municipality

- A 10% reduction in the number of STR zoning rights per two years

- An auctioning off of the remaining STR zoning rights per two-year licence

- The revenue raised from such development rights be delivered to local councils to fund perpetually affordable housing, such as Community Land Trusts.

The report outlines the advantages of this system over the 90 day cap, with a closed loop system redirecting STR profits towards the funding of affordable housing.

Ninety days caps cut deeply into the STR industry, threatening investments made at today’s ridiculously high prices. The cap ‘n trade system gives STR investors time to redeploy their investments over time. Such a system also allows the market to reorient those resources based on the personal preferences of investors. Will they be able to afford an $8,500 licence fee in a few years time?

Principles for the STR Cap ‘n Trade system would include:

- A two-year implementation window to assist the phase in

- A preference for purpose built STRs that do not remove housing from the market

- Only those investors with the STRA would be permitted to commercially operate.

- The statewide, standard fee structure would offer uniformity and certainty for operators, as would the two year timeframe.

- This fee would supersede local government STR fees.

- Enforcement would be accompanied by significant fines worthy of 25% of annual STR incomes.

- The licences could be structured according to dwelling size, to ensure family sized homes are not lost to the STR market.

- Some short term letting is acceptable without a licence i.e. a person renting out a home whilst they are on annual holiday for a short period of time.

The zoning provided would prioritise new dwelling supply into STR. Existing dwellings should be discouraged from entering this market. An appropriate incentive charging a higher licence fee of some 25% could be utilised for existing dwellings. This would increase by 50% for STRs in pre-existing dwellings within 1km of a town centre.

The use of commercial buildings could be incentivised in the work-from-home world we now live in. Commercial STR operators producing new dwellings at a commercial location therefore would pay the standard rate.

The Federal government could also prioritise local communities by:

- Reducing the CGT discount to 25% for STR properties

- Removing the CGT exemption for small businesses with STR holdings

- Disallowing SMSF borrowings for the purchase of STRs

- Curbing accelerated depreciation for STRs.

Importantly, the cap ‘n trade system shares the STR bounty with local communities, with a push to use the funding for much needed affordable housing. Grounded advocates that Community Land Trusts are the most effective means of providing this. This is due to their ability to cap housing access to the growth in our wages. Over time, this model will be proven as the best at maintaining any public subsidy and using it to scale up affordable opportunities. That’s why we call CLTs the gold standard in shared equity.

With sprawl concerning many communities, it is vitally important that government considers whether master planned development is the way to deliver affordability. For-purpose developers can provide directly affordable outcomes, whereas the typical development model requires some 1000 lots to deliver what one CLT can provide in 40 lots.

Let’s hope we can convince government to cap STR numbers and establish a licensing system to fund affordable housing.