Submission to the NSW Short and Long Term Rental Inquiry

Grounded Community Land Trust Advocacy is an NGO focused on bringing Community Land Trusts to fruition. CLTs are a form of shared equity where the Trust maintains ownership over the land to ensure perpetual affordability occurs. Residents need only borrow for the improvements, ensuring the deposit required is just 40% of the open market, with similar borrowing advantages possible. Importantly, they close the loop on government subsidy through an affordability lock.

The “Locals First” AirBnB policy

Introduction

Communities need a say on what constitutes a reasonable percentage of visitor accommodation in their community. For too long we have let the market decide. The results for those who may have missed out on the property game have been harrowing.

The increasing mobility of capital, alongside the professionalisation of property management, property styling and proptech has seen rapid change thrust upon many New South Wales communities. When short term rentals (STR’s) are added to the pressures of holiday homes in curtailing the supply available to a community, the affordability impact requires deeper study.

AirBnB returns are significantly outperforming the rental market, incentivising investors to switch supply into this unregulated field. “When compared to a long-term rental on Domain.com.au for a similar property advertised at $700/week, the MadeComfy property outperforms by 60.1% in the six months to March 2023.”

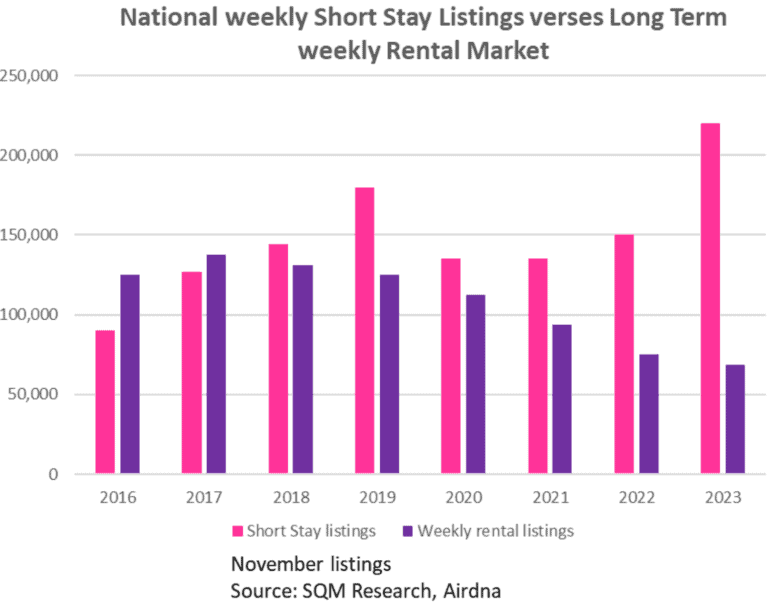

Figure 1

As long as the market can deliver higher returns to investors in short term holiday letting, these properties are highly unlikely to return to the long term private rental market.

Many tier one tourism hot spots barely require a 50% occupancy rate to make a 200% return on the long term rental market:

- Byron – $122K median revenue per property, 58% occupancy (median annual rent $65,000)

- Shoalhaven – $80k revenue, 46% occupancy (median annual rent $30,680)

- Coffs Harbour – $70K revenue, 53% occupancy (median annual rent $32,760)

Similar outcomes are occurring in tier 2 towns such as:

- Parkes – $58K revenue, 58% occupancy (median annual rent $21,840)

- Yass – $60k revenue, 43% occupancy (median annual rent $28,600)

- Orange $67k revenue, 57% occupancy (median annual rent $27,144)

If these returns continue, the LTR shrinkage will continue as per Figure 1.

With such lucrative returns, the 60 day cap still allows new supply to head straight to STR. Will mooted granny flat reforms again rob supply and more precious days, months and years from those living precariously?

Victoria’s AirBnB levy, whilst admirable for innovating outside of the 60 day cap on STR’s, will be passed onto tourists as many locations do not have a significant hotel nearby to outcompete them. Such a levy will however have a marginal impact on the site’s land value.

Government must recognise that AirBnB returns have had a significant impact on rental supply, particularly in tier 1 tourism towns. The state must mobilise to enact planning law that prioritises the rights of local communities first.

An AirBnB Cap & Trade Policy

The Locals First policy would develop a Long Term Rental supply objective compared to the present situation. A three year median of rental supply is to be calculated (preferably pre 2012, when AirBnB arrived).

A pathway would then be drawn between the two, aiming to return long term rental supply near to where it was circa 2010 – 12, relative to population growth.

NSW would be required to create a zoning for short term rentals. This would deliver a Short Term Rental Agreement (STRA) between planning and the landlord. The NSW Independent Planning Commission recommends such a reform in its Byron Short-Term Rental Accommodation Planning Proposal:

“Defining STRA as a permissible use by specifically listing STRA as a type of ‘tourist and visitor accommodation’ with the objective of facilitating STRA in well located and serviced areas already zoned for tourism.”

Non-hosted STRA must be zoned.

This STRA zoning right would then be auctioned off for a 3 year licence. Only those investors with the STRA would be permitted to commercially operate. Enforcement would be accompanied by significant fines worthy of 25% of annual STR incomes.

Figure 2

Figure 2 shows how the cap and trade aspect of the Locals First system would work. Each year the number of STRA applications would fall by some 10%. Over time the economic rent of the STRA in Byron Shire, currently at some $57,000, would be bid towards the STRA zoning licence. The STRA bids would continue until the surplus economic rent converged towards the $65,000 in LTR income.

As the opportunity costs narrow, the trajectories evident in Figure 1 would reverse.

How significant could those revenues be?

In Byron Shire the potential in STRA licensing is $87.5m per annum and climbing. Currently, some $199.5m is leaving the shire each year in economic rents enjoyed by AirBnB landlords.

Over time, as the amount of STRA zoning rights is tapered downwards, more stock would be freed up for rental. By doing this over time, AirBnB investors will have space to switch their focus.

A related precedence exists in Sao Paolo, where the auctioning of development rights occurs.

The revenues would be hypothecated towards perpetually affordable housing. This would preferably support the emergent Community Land Trust sector so that permanently affordable housing could gain a foothold.

We feel this policy would have a more immediate and direct impact on rental supply than an AirBnB levy or 60 day cap. A 60 day cap, whilst reducing incomes marginally if at all, does not curb STRA supply levels with the immediacy the current housing market requires. STR prices may simply increase.

Current supply outcomes

Over the decade to 2021, local dwelling supply in Byron Shire increased by 2,460 dwellings. AirBnB supply increased by 3,500.

With governments under pressure to add to supply, including via granny flats, the use of such secondary dwellings as STR’s could still occur. This will not put downward pressure on LTR rents.

Having the STRA cap in place under the Locals First policy would ensure that granny flats would likely add to the much needed LTR supply required for single person dwellings.

STRA licensing prices could also be varied according to size, so that it did not favour larger party sized homes who could outbid smaller homes. Affordable rental supply for families need not be further undermined.

Consolidation in AirBnB management

Some oversight is necessary to measure the extent of market power enjoyed. It appears there are two cohorts of AirBnB landlords – those that own 1-2 properties and those that own 10+.

Private equity firm Next Capital has recently purchased Allogio for $48m for the management rights to 2220 STRAs along the east coast. They provide the property management services of ‘all of the housekeeping and the gardening and the pool maintenance and the accounting and the reservation communication on behalf of holiday homeowners.’

In Coffs Harbour, Next Capital manages 15.8% of AirBnB listings. In Byron Bay, via their $11m purchase in A Perfect Stay, they manage 4.3% of listings. It is unclear how many of these are owned outright.

The data in Victoria demonstrates similar market power. In Colac Otway, Great Ocean Road Holidays manages 153 out of 916 STRs – 16.7% of the market. In Barwon South West, Great Ocean Road Holidays manages 450 STRs – 20.9% of the market. The parent company behind Great Ocean Road Holidays was Allogio Group.

Whether STRA agreements incorporate property management rights is a factor to consider. We can expect as this market matures that further consolidation will occur, particularly in ownership. The steady management rights enjoyed by Next Capital would allow deeper relationships with a financier to occur, adding potential for further leveraging and the purchasing of STR properties outright. Indeed, a private equity capital raising is more likely to occur.

Vacant Land and Housing

Vacant land and housing taxation was raised in the discussion paper and is certainly worth mentioning. Current policy settings have dismembered the most powerful tool in NSW’s housing affordability kit. The state’s indexation of land tax thresholds to the median land value is damaging. It implies that the higher land values reach, the more (once) affordable land is released from its land tax burden. As economic theory would dictate, that ensures the land price will continue to escalate. Why? Because it encourages investment activity to focus on these locations. Recent PEXA findings reveal that ¼ of residential purchases in NSW were entirely in cash. “The places with the highest proportion of cash purchases were in regional areas popular with older Australians who are likely to be retired…”. Zero land tax places a target on these locations, the last remaining NSW communities where affordable housing is possible.

The first and most important step to the NSW government moving towards a fairer housing market is to remove the indexation of land tax thresholds. This will push under-performing STRs back towards the LTR market. Land tax is the most effective form of vacancy tax available.

Conclusion

A recent AirBnB-funded report, this time by Urbis, again adopted the strategy of watering down the influence of STRs. This tactic was used in the previous AirBnB study performed by SGS Economics (2018). Both reports compared STRs to the total housing market, rather than the rental market itself.

Unsurprisingly, they found it “has “no consistent impact” on housing affordability, only accounting for 1% to 2% of dwellings …..But [Guardian analysis finds] 1% to 2% of all dwellings is about 3% to 7% of rental properties.”

Such 100+ page reports costing several $100,000 must compare STRs to the rental market, particularly at a regional level.

If this strategy was used to analyse Tier 1 tourism regions, the impact of STRs is alarming. We compared STR’s to LTRs across the LGAs of the following communities:

- Byron Bay: 66.2% of rental supply

- Shoalhaven: 36.1% of rental supply

- Coffs Harbour: 15.5% of rental supply.

Further, if we look at the influence of profit driven investment, STR’s as a percentage of new supply is substantial:

- Byron Bay: 142.3% of new supply created was absorbed by STRs

- Shoalhaven: 72.5% of new supply created was absorbed by STRs

- Coffs Harbour: 35.2% of new supply created was absorbed by STRs.

These are headline figures only, with intra-market substitution likely occurring. However, it identifies a trend that we know so well. Investment will follow the money.

Government must do better in employing economic futurists who can predict supply outcomes relating to these simple economic drivers.

STR landlords of Byron Bay, Shoalhaven and Coffs Harbour are enjoying economic rents of $513m p.a. How extensive are the economic benefits throughout the state? Are these economic returns commensurate with the net value these lettings provide the local economy?

This submission presupposes that at least $1bn could be raised from the licensing of short term lets. This money should be hypothecated towards Community Land Trusts as these provide perpetually affordable housing that can close the loop on government subsidy so that scale can be achieved.

It is time the NSW government provided a clear and direct path to regulate a Short Term Rental industry that enjoys considerable economic returns.

The Locals First policy delineates the problem in black and white and provides a clear pathway back towards long term rentals. This can be achieved by determining STR economic returns are equivalised to LTR returns.

Tourism towns deserve the right to ensure the long term survivability of their town.

The number of AirBnB sites must be capped and traded downwards to ensure a fairer distribution of housing occurs. This will allow the liveability that initially attracted people to a tourism hotspot to once again flourish so that joy spreads to both visitors and locals.